Audrey Galawu

Assistant Editor

The overall regulatory environment in the mining sector in Zimbabwe is not conducive with multiple and overlapping processes from different agencies.

Licensing requirements in Zimbabwe remain costly and burdensome, said the National Competitiveness Commission in the 2023 report.

For instance, application for an investment license at the Zimbabwe Investment and Development Agency is US$500 and issuance of an investment license upon approval is US$4 500.

As at December 31, 2023, Zimbabwe had the highest application and investment fees as compared to other countries such as South Africa (US$150), Zambia (US$560), Rwanda (US$500), Malawi (US$1 000) and Botswana (US$152).

In comparison to other countries like Rwanda where investment licenses pay nominal fees of US$500, Zimbabwe becomes an unattractive investment destination.

According to the Zimbabwe Statistics Agency report, the mining sector experienced positive growth since 2020, which enhances the country’s competitiveness, with highest growth recorded in 2022.

However, there was a notable decrease of growth rate to 4.8% in 2023 attributed to low international commodity prices, high-cost structure, foreign currency shortfalls, among other factors.

“This growth in the mining sector improves the economy of Zimbabwe as it attracts foreign investors who will bring foreign currency thereby increasing the country’s income. Furthermore, foreign investors bring technical expertise into the country thus improving competitiveness.

“In terms of export revenue from the mining sector, the country is recording significant improvement as receipts are increasing on average.

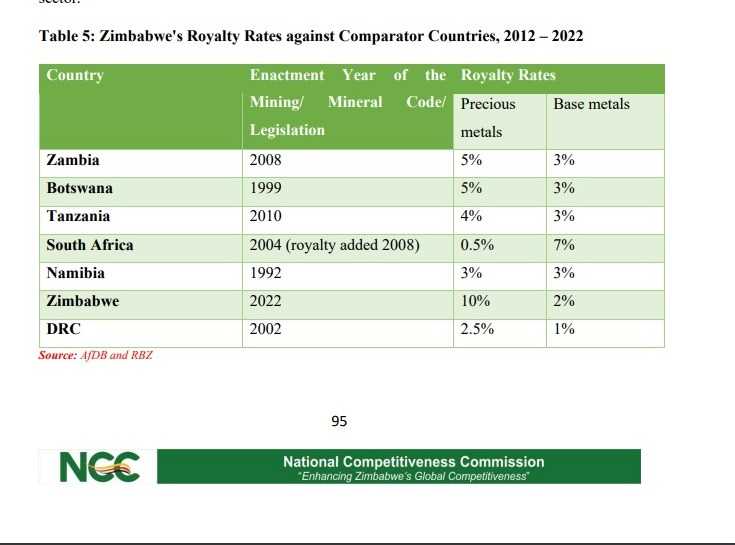

In terms of royalties, the NCC has argued that Zimbabwe charges the highest rate on precious metals (10%) compared to comparator countries, which makes it less competitive in attracting both domestic and foreign investment. Investors prefer relatively lower rates than higher rates.

Related Stories

“On the other hand, royalties on base metals are relatively competitive (2% for Zimbabwe) compared to other countries except for DRC which is charging 1%,” reads the report.

The report highlights that the country needs to consider both investor attractiveness particularly in mining of precious minerals and striking a balance with revenue collection.

“Regardless of having tax incentives in the mining industry the cost of production increased by 10% between 2022 and 2023 due to electricity tariff increase, high cost of funding, high labour costs, high royalty and taxes. This means there is need for Government to adjust on electricity tariffs, labour laws, royalty and taxes to be favourable to attract foreign investors.

“Some of the regulations implemented are making the mining sector less competitive as they are increasing the costs of production. This is also exacerbated by decrease in international prices, which reduces revenues that are even not even covered by an increase in production.”

The rise in electricity costs by USc2/ KWh in October 2023 has resulted in the cost of production increasing by 10%. In addition, the increase in royalty for PGMs (2.5% to 7%) and Lithium (2% to 7%), resulted in the overall cost of production rising by an average of 5% and 4%, respectively.”

This reduces the competitiveness in the mining industry as high costs will be incurred, which reduce revenue as well as profits, negatively impacting on investors’ interest in the mining industry.

The Zimbabwe Investment and Development Agency report for Q2 2024, however, has recorded the mining sector to be the sector with the highest number of licenses issued totalling 65 out of 154, with a Projected Investment Value of US$282.74 million.

Zimbabwe, however, is competitive regarding the zero percent customs duty on capital goods that miners may import into the country.

Whilst a miner is still required to pay value added tax on various mining equipment, this can be deferred for a maximum period of three years, depending on the value of equipment.

“This means that a miner can import capital equipment into the country for use in their exploration and mining endeavours at very low costs (without paying VAT immediately) thereby ensuring that the country has a competitive edge with regards to mining.

“Moreover, mining companies enjoy an indefinite carry-forward of their tax losses. Investors are permitted to borrow locally for working capital purposes while offshore borrowings require RBZ approval. Interest paid on borrowings of a debt-to-equity ratio of up to a maximum of three years to one year is tax deductible.”

Leave Comments