Zimbabwe's manufacturing sector remains heavily dependent on imported raw materials, a structural weakness that industry leaders say is driving up production costs, eroding competitiveness and undermining efforts to build a resilient industrial economy.

New findings from the Confederation of Zimbabwe Industries Manufacturing Sector Survey 2025 show that several key manufacturing subsectors source the majority of their raw materials from outside the country, exposing producers to exchange rate volatility, foreign currency shortages and global supply chain disruptions.

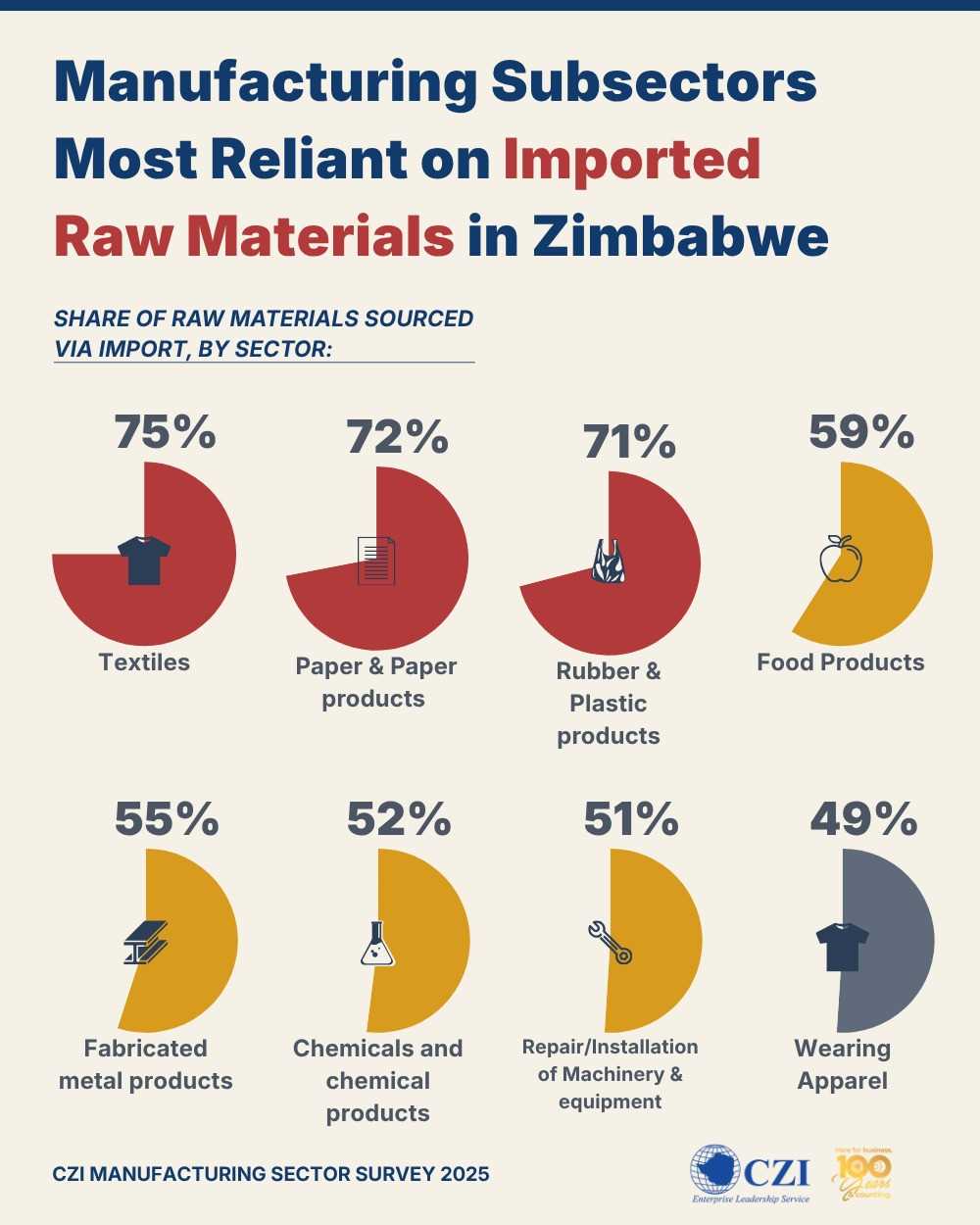

According to the survey, the textile sector is the most import-dependent, sourcing 75% of its raw materials externally. Paper and paper products follow at 72%, while rubber and plastic manufacturers import 71% of their inputs. The food processing sector, one of Zimbabwe's largest manufacturing employers and a critical component of national food security, relies on imports for 59% of its raw material requirements.

Fabricated metal products source 55% of their inputs from foreign markets, chemicals and chemical products import 52%, while machinery repair and installation businesses depend on imported materials for 51% of their operations. Even the wearing apparel sector, which has traditionally been viewed as a potential driver of local value addition, imports nearly half of its raw material requirements at 49%.

The survey findings underscore the scale of the challenge facing policymakers seeking to promote local content, industrialisation and import substitution under Zimbabwe's industrial development agenda.

"Heavy reliance on imported raw materials continues to shape production costs and competitiveness in Zimbabwean manufacturing," CZI said in releasing the survey findings.

The figures come at a time when Government is intensifying efforts to strengthen local value chains. Earlier this week, Industry and Commerce Permanent Secretary Ambassador Thomas Chifamba toured National Foods, where discussions focused on local content development, value addition and accelerating the Buy Zimbabwe campaign.

However, the latest data suggests that despite years of policy commitments to industrialisation, much of Zimbabwe's manufacturing sector remains dependent on foreign suppliers for critical inputs.

The implications extend beyond production costs. Manufacturers that rely heavily on imported raw materials must secure foreign currency to sustain operations, making them vulnerable to exchange rate fluctuations and liquidity constraints. These pressures are often passed on to consumers through higher prices, reducing the competitiveness of locally produced goods against imports.

CZI chief executive officer Sekai Kuvarika has previously argued that the country's industrial competitiveness challenge begins with weaknesses in domestic supply chains.

Related Stories

"Competitiveness means addressing primary production so that processing becomes competitive and we begin to reduce import dependency. Nearly 60% import reliance in food manufacturing is significant and must be addressed."

The food processing sector's dependence on imports is particularly striking given Zimbabwe's agricultural potential. While the country produces maize, wheat, soya beans and other agricultural commodities, manufacturers continue to import substantial quantities of raw materials due to supply gaps, quality requirements and production shortfalls.

The textile industry presents an even starker example of industrial decline. Once a major employer with a fully integrated value chain stretching from cotton production to garment manufacturing, the sector has seen many companies either close or scale down operations over the past two decades. The result has been increased dependence on imported fabrics, yarns and other inputs.

The findings also raise questions about the effectiveness of import substitution policies that have featured prominently in government economic blueprints. Economists note that while local production has expanded in some sectors, the inability to develop domestic suppliers of intermediate goods means that significant portions of the value chain remain externalised.

This dependence has persisted despite repeated policy interventions.

Previous CZI surveys have consistently shown import dependency levels exceeding 50% across manufacturing, indicating that structural challenges remain largely unresolved.

Industry leaders have long argued that reducing import dependence requires more than protective policies. They point to the need for increased investment in agriculture, chemicals, packaging, engineering and other upstream industries capable of supplying manufacturers with competitively priced local inputs.

The challenge is occurring against a backdrop of declining manufacturing capacity utilisation. Recent CZI surveys show that capacity utilisation has fallen in recent years as firms grapple with high operating costs, power shortages, regulatory burdens and limited access to affordable financing.

Kuvarika has previously warned of the broader consequences for industry.

"We are trending towards de-industrialisation."

The warning reflects concerns that without stronger domestic value chains, Zimbabwean manufacturers will struggle to compete both locally and internationally. High import dependence not only increases production costs but also limits the sector's ability to retain value within the economy, create jobs and generate sustainable industrial growth.

Leave Comments