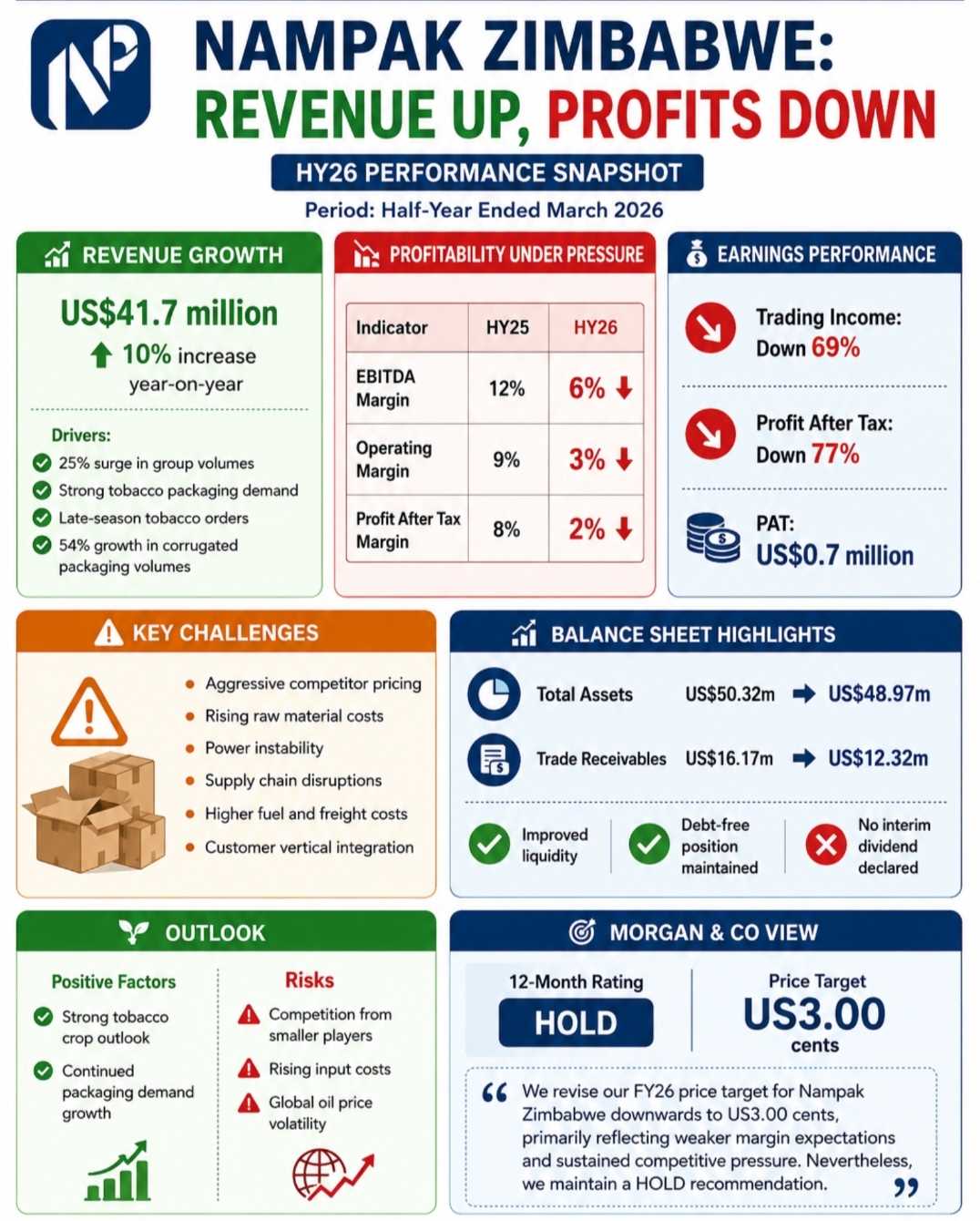

Nampak Zimbabwe recorded a 10% increase in revenue during the first half of its 2026 financial year, driven by stronger demand across its tobacco packaging and corrugated packaging businesses.

However, the growth failed to translate into improved profitability as shrinking margins, rising costs, and operational challenges weighed heavily on earnings.

According to a latest equity research note by Morgan & Co, the packaging manufacturer posted revenue of US$41.7 million for the six months ended March 2026, up from the comparable period last year.

The growth was largely supported by a 25% increase in volumes from the tobacco packaging division and a recovery in demand from tobacco-related sectors.

"Revenue increased by 10% to US$41.7 million, supported primarily by a 25% surge in group volumes from strong tobacco packaging demand and the carryover of late-season tobacco orders," Morgan & Co said.

The brokerage noted that while the Printing and Converting business benefited from former tobacco-related demand, the Corrugated Packaging division saw volumes increase by 54% due to improved demand in the commercial packaging segment.

Despite the top-line growth, profitability deteriorated significantly. Operating profit declined to 4% from 8% in the prior period, while earnings before interest, tax, depreciation and amortisation (EBITDA) margins weakened to 6% from 12%.

"Despite stronger volumes, aggressive competitor pricing and raw material cost inflation significantly compressed margins," the report said.

Related Stories

Morgan & Co added that operating margins narrowed to 3% from 9%, while profit after tax fell to 2% from 8%. Trading income declined by 69% and profit after tax dropped by 77% to approximately US$0.7 million.

The research firm said Nampak's balance sheet continued to improve, with total assets easing to US$48.97 million from US$50.32 million as working capital efficiencies and tighter inventory management helped preserve liquidity.

"Working capital dynamics improved during the period, with trade receivables reducing materially while liquidity was supported by inventory management initiatives," Morgan & Co noted.

However, the company retained debt-free status and did not declare an interim dividend as it prioritised capital expenditure requirements.

Looking ahead, Morgan & Co expects demand from Zimbabwe's tobacco sector to continue supporting packaging volumes, particularly in corrugated and tobacco-related packaging. Nevertheless, the brokerage warned that competition from smaller, more efficient operators, together with high input costs and fuel-related expenses, could continue to suppress margins.

"The 2025/26 tobacco crop outlook is expected to support packaging demand through the second half. However, persistent competition from smaller and more efficient players, customer vertical integration, power instability, and rising raw material input costs are expected to continue weighing on margins and earnings recovery," the analysts said.

The firm also highlighted global geopolitical risks and elevated oil prices as factors that could further increase freight, resin and fuel-related costs.

As a result, Morgan & Co revised its valuation for the company downward and maintained a cautious stance on the stock.

"We revise our FY26 price target for Nampak Zimbabwe downwards to US3.00 cents, primarily reflecting weaker margin expectations and sustained competitive pressure. Nevertheless, we maintain a HOLD recommendation," the brokerage said.

The analysts noted that ongoing discussions surrounding Nampak SA's stake in the Zimbabwean unit could provide a potential corporate action catalyst for the counter, even as operational headwinds persist.

Leave Comments