Zimbabwe's financial sector is entering a new phase in which banks and pension funds are being forced to adjust to an operating environment in which profits can no longer be driven by inflation, exchange-rate volatility and property revaluations.

Industry players warn that the country's tight monetary policies are simultaneously constraining credit growth and exposing structural weaknesses in long-term savings.

Annual statements by ZB Financial Holdings and FBC Holdings, together with a new research report by Streetwise Economics, suggest that the macroeconomic stability achieved through tight monetary and fiscal policies has fundamentally changed the way financial institutions generate earnings.

While the policies have succeeded in stabilising the Zimbabwe Gold currency and reducing inflation, they have also reduced the foreign exchange and fair value gains that had boosted bank profits during periods of currency instability, while exposing pension funds whose asset values remain heavily reliant on property revaluations.

ZB Financial Holdings warned that although the Reserve Bank of Zimbabwe's tight monetary policy had helped maintain exchange-rate and price stability, high statutory reserve requirements and the policy rate, which stood at 35 percent before it was reduced to 30 percent this week, had constrained credit growth and reduced banks' lending capacity.

The group said authorities may eventually need to recalibrate policy measures to balance macroeconomic stability with increased private sector investment and economic growth.

"While these measures supported currency stability, they also constrained credit growth, limiting the banks' lending capacity," ZB Financial Holdings chairperson Agnes Makamure said.

FBC Holdings echoed the concerns, saying the prevailing monetary and fiscal stance had created funding constraints that were limiting the banking sector's financial intermediation role. The group said banks were increasingly relying on foreign lines of credit to supplement domestic funding for lending activities.

Despite those challenges, both institutions acknowledged that Zimbabwe's macroeconomic environment improved significantly during 2025, with economic growth accelerating to 6.6 percent, supported largely by agriculture and mining. They also credited tighter monetary policy with reducing inflation and stabilising the ZiG exchange rate.

However, the same stability has brought an end to the sizeable foreign exchange and fair value gains that had previously inflated financial sector earnings.

ZB Financial Holdings reported that profit after tax declined to ZWG0.679 billion from a restated ZWG1.042 billion in 2024, largely because exchange gains declined following the stabilisation of the ZiG. The group said its core operating earnings nevertheless improved.

FBC Holdings also recorded a sharp decline in revaluation and fair value gains but reported stronger underlying operations, with profit before tax increasing 84 percent to US$31.4 million and profit after tax rising 69 percent to US$30.4 million, driven by stronger lending, transaction volumes, fee income and disciplined cost management.

A new report published by Streetwise Economics suggests that while banks have largely adjusted to the new environment by relying more on operational income, pension funds remain significantly exposed to declining property revaluation gains.

The report found that 44.1 percent of Zimbabwe's pension assets, equivalent to US$1.16 billion as at June 30, 2025, remain invested in property, yet these assets generate rental yields of only about 3.7 percent annually, well below the estimated 12.4 percent cost of capital.

Related Stories

According to the report, during periods of currency instability, rising property valuations generated substantial accounting gains without producing corresponding cash income. As the ZiG stabilised through 2024 and 2025, those gains slowed sharply.

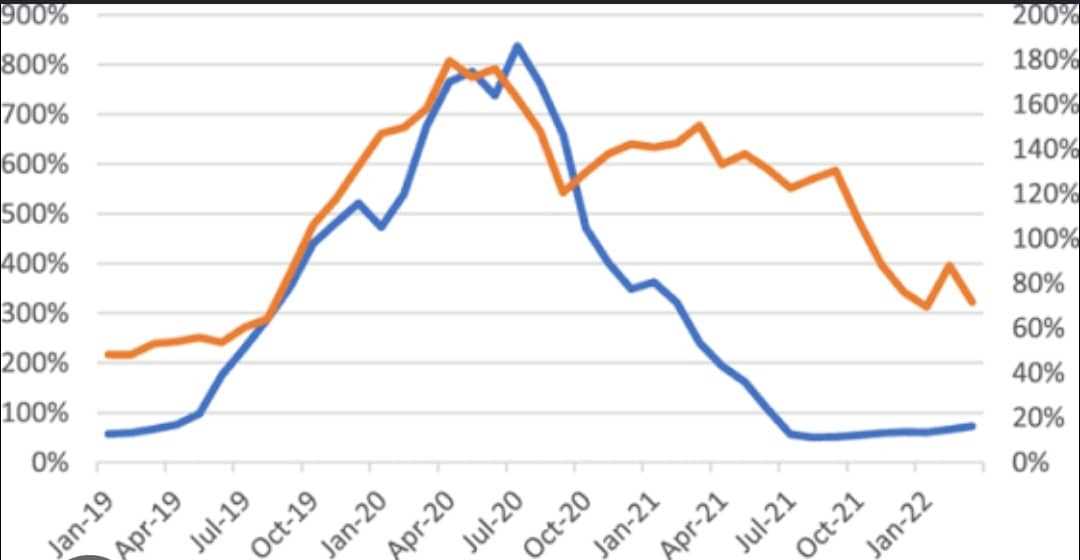

The study noted that paper gains from property and foreign exchange revaluations accounted for about 61 percent of banking sector income in early 2024 before falling to roughly six percent by early 2025. During the same period, sector return on assets declined from 22.8 percent to 2.4 percent, revealing weaker operational profitability after revaluation gains faded.

The report said the shift had laid bare the banking sector's underlying earnings capacity.

"The paper gains had been flattering the numbers; when they faded, how thin the operational earnings were underneath became visible. The banks that came through the reversal well are the ones that earn from lending, not from marking up property," the researchers said.

The researchers said pension funds have yet to undergo a similar adjustment.

The report found that total pension sector income declined by 78.7 percent during the first half of 2025 as property revaluation gains slowed in response to greater currency stability, indicating that previous earnings had been heavily supported by unrealised valuation increases.

Streetwise Economics further warned that pension members bear significantly greater risk than bank shareholders because they cannot easily exit their investments.

The report argued that the burden of any correction would fall disproportionately on ordinary workers.

"When a pension's property re-prices, the loss falls on members — people who never chose the exposure, cannot exit it, and in many cases are already drawing benefits calculated against the inflated asset base," the report said.

The report noted that the average pension benefit stood at approximately US$30 per month in 2024 despite pension funds holding more than US$1 billion in investment property. It added that nearly one million Zimbabweans are members of occupational pension schemes, while more than 100,000 members were owed unclaimed benefits by mid-2025.

The report also modelled the potential impact of repricing pension property to reflect higher market yields.

Its analysis estimated that valuing property at a six percent yield would result in a 38 percent write-down in property values, while using the full 12.4 percent cost of capital would imply a decline of up to 70 percent, reducing total pension sector assets by about 31 percent. The report stressed that these scenarios represent stress tests rather than predictions of an imminent market correction.

The researchers also highlighted broader structural challenges, noting that prescribed assets accounted for only 10.4 percent of pension portfolios, well below the statutory 20 percent minimum, increasing pressure on fund managers to deploy capital into assets that may not generate adequate cash returns.

Both the banking institutions and the research report point to the same conclusion: Zimbabwe's financial sector is increasingly shifting away from dependence on inflation, exchange-rate movements and asset revaluations towards earnings generated from lending, transaction banking and other core financial services.

While banks called for a policy balance that preserves macroeconomic stability without excessively restricting private sector credit, the Streetwise Economics report recommended stronger disclosure requirements for property valuations, annual stress testing of pension assets, and closer coordination between the Insurance and Pensions Commission and the Reserve Bank of Zimbabwe in monitoring property-related financial risks.

Leave Comments