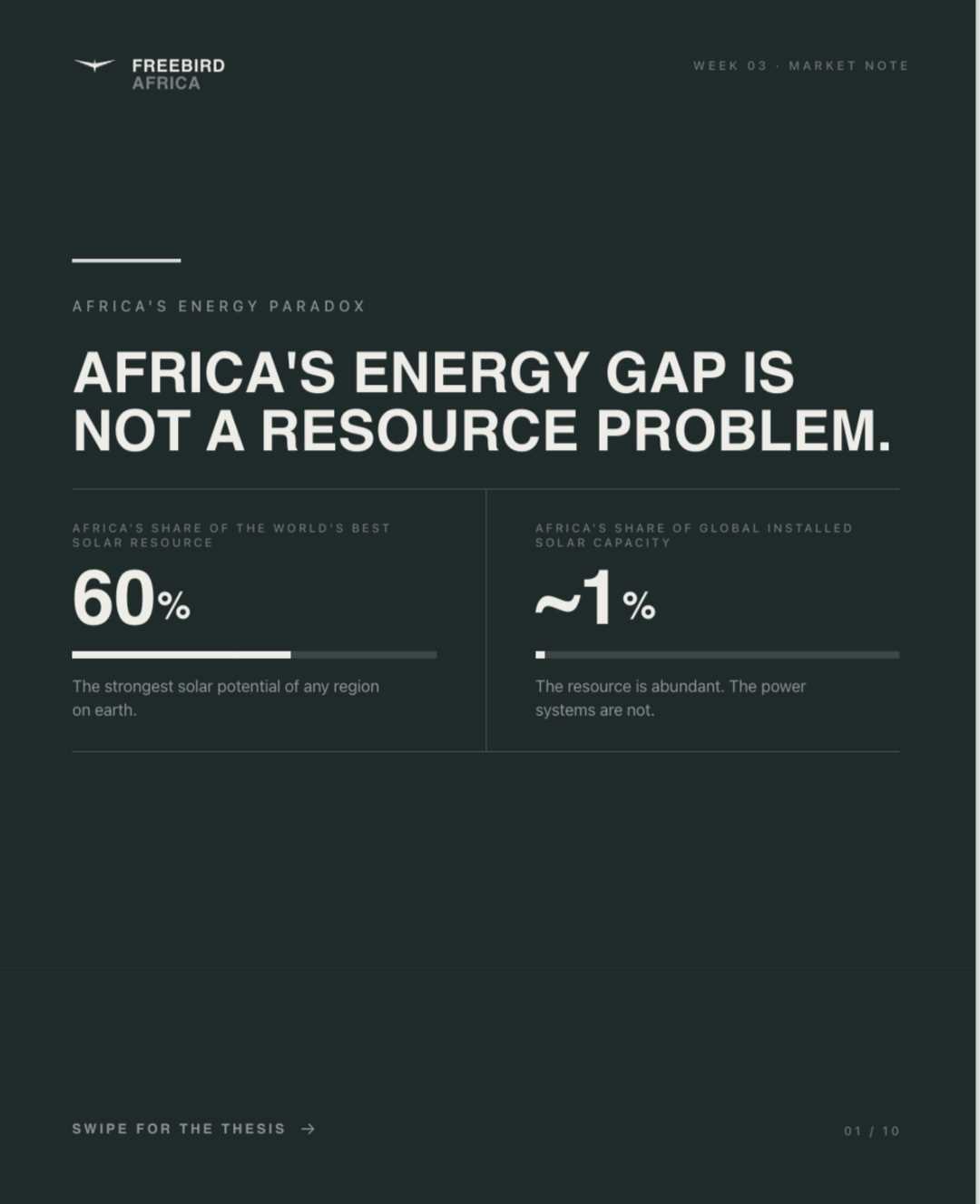

Although Africa possesses 60% of the world’s best solar resources, it accounts for only around 1% of global installed solar capacity.

As nations across East and Southern Africa pursue ambitious industrial and mining growth, a fundamental challenge persists: a widening "readiness gap" between the region's vast natural resource potential and its constrained power infrastructure.

In Zimbabwe and Zambia, this vulnerability was starkly exposed in 2024 when severe drought significantly reduced hydropower generation, leaving critical mines and industries facing major electricity shortages. The regional instability has highlighted the urgent need to move beyond traditional energy models towards diversified systems that include energy storage, captive power solutions and stronger regional transmission networks.

The Energy Paradox: Abundance Versus Infrastructure

Although Africa possesses 60% of the world’s best solar resources, it accounts for only around 1% of global installed solar capacity. Experts argue that this imbalance is not due to a lack of resources, but rather a shortage of adequate infrastructure.

Energy remains the foundational layer of economic development. Without reliable and affordable electricity, many investments in mining, mineral processing and manufacturing struggle to progress beyond the planning and feasibility stages.

Power as the Foundation of Industrial Value Chains

A recent market note by FreeBird Africa identifies energy as the first and most critical link in the industrial value chain. The report argues that electricity infrastructure should be treated as a prerequisite for development rather than an afterthought following resource discoveries.

The value chain begins with power generation through national grids, captive power plants and renewable energy systems. It supports mine operations, including extraction and haulage, enables beneficiation and refining to retain more value within African economies, and underpins the transport and logistics systems required to move products to global markets.

Industrial energy demand, including requirements from freight transport and agriculture, is projected to rise by nearly 40% by 2030, reflecting the region’s broader push toward industrialisation and local value addition.

The Capital Investment Challenge

Related Stories

Despite Africa’s vast potential, the continent currently attracts only about 3% of global energy investment. Analysts say the main obstacle is not a lack of ambition, but a shortage of well-structured, investable projects.

Meeting Africa’s energy development goals will require annual investment to increase nearly fivefold, from approximately US$40 billion in 2024 to an estimated US$190 billion annually from 2026 onwards, with around two-thirds of this funding directed towards clean energy.

Investors generally finance bankable projects rather than resource deposits alone. Without reliable power supply and access to transmission infrastructure, even high-quality mineral resources may struggle to attract financing.

However, opportunities remain significant. Large industrial consumers, such as major copper producers, can act as anchor customers by providing predictable demand and financial credibility, helping new renewable energy projects secure investment.

Regional Energy Realities

The energy challenge varies across African markets.

Kenya relies heavily on geothermal power for baseload generation.

Tanzania combines natural gas and hydropower resources.

Uganda remains dependent on hydropower and regional electricity trade.

Mozambique benefits from natural gas reserves and strategic coastal access.

Zambia and Zimbabwe continue to balance growing mining demand with increasing exposure to hydrological risks.

The transition towards cleaner and more resilient energy systems is increasingly becoming a matter of economic development, competitiveness and operational security rather than simply achieving emissions targets.

Leave Comments