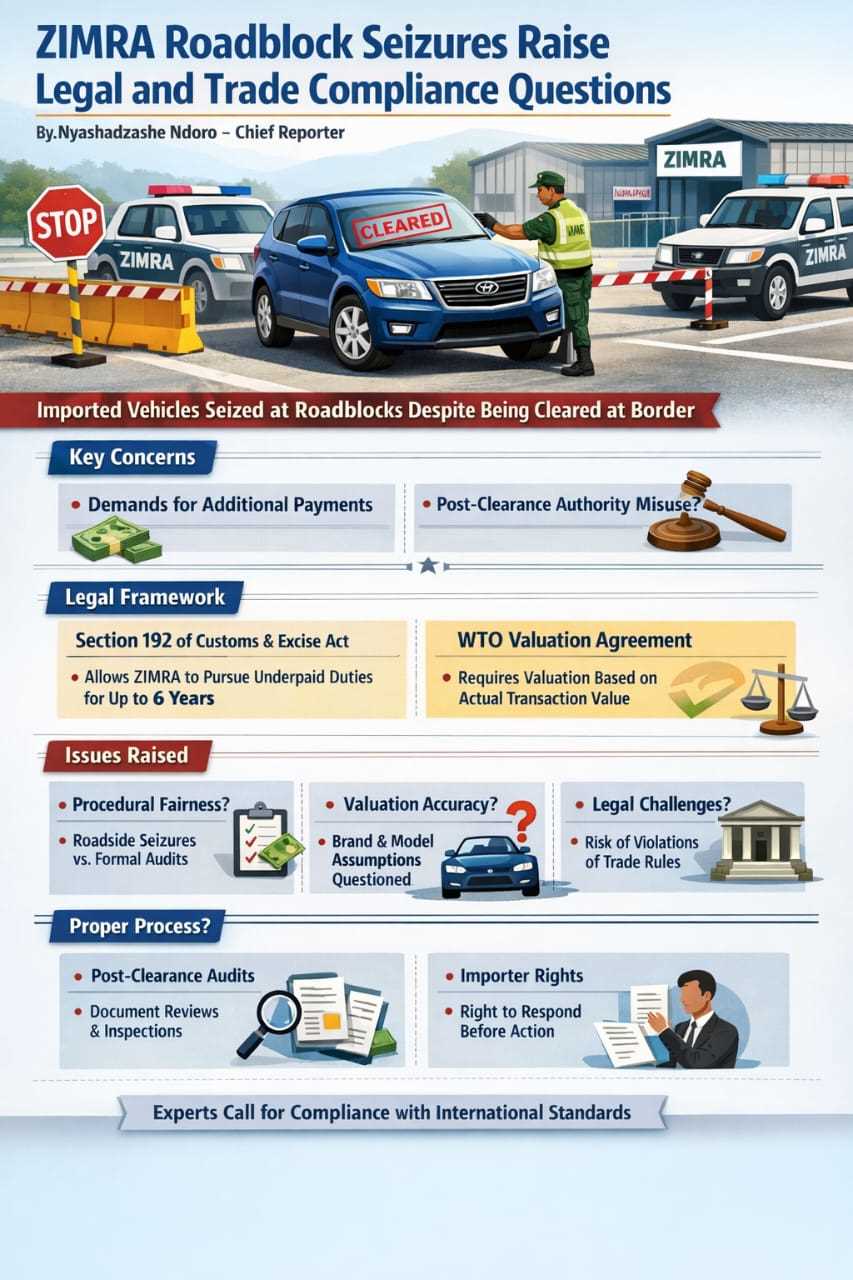

Concerns are mounting over reports that the Zimbabwe Revenue Authority is stopping and seizing already-cleared imported vehicles at roadblocks, particularly high-value units whose duties were paid and registration completed at the point of entry.

Affected motorists and industry observers say some vehicles are being detained or only released after additional payments are demanded, despite having undergone formal customs clearance procedures at the border.

The developments have triggered debate within trade and customs circles, with professionals such as Vincent Mutsvene weighing in on the legality and procedural correctness of the enforcement measures.

At the centre of the issue is Section 192 of the Customs and Excise Act, which grants ZIMRA the authority to pursue underpaid duties for up to six years after goods have been cleared. Analysts note that this provision gives the tax authority broad post-clearance powers, and its existence is not in dispute.

However, questions are being raised about how those powers are being exercised in practice.

Related Stories

Zimbabwe is a member of the World Trade Organization (WTO) and is bound by the Customs Valuation Agreement under GATT Article VII. The agreement requires customs authorities to determine the value of imported goods using a strict sequential hierarchy of six methods, beginning with the actual transaction value.

Trade experts argue that any deviation from this method must be supported by objective and verifiable evidence, a process typically conducted through document reviews rather than on-the-spot assessments.

“There is a distinction between having legal authority and applying it correctly,” one customs expert said, noting that valuation reassessments require detailed analysis that cannot reasonably be conducted at roadside checkpoints.

The WTO framework also prohibits the use of arbitrary or minimum customs values. Analysts warn that if enforcement practices rely on assumptions about a vehicle’s value based on brand, model, or perceived prestige, this could conflict with international obligations.

Domestically, the Customs and Excise Act provides for a structured post-clearance audit process under Sections 223A to 223C. This framework outlines procedures such as document reviews, premises inspections, issuance of written findings, and granting importers the right to respond before any enforcement action is taken.

ZIMRA’s own administrative guidance describes post-clearance audits as corrective and educational in nature, aimed at ensuring compliance rather than imposing immediate penalties.

Critics argue that seizing vehicles at roadblocks before completing this process risks undermining procedural fairness and could expose the authority to legal challenges.

Leave Comments