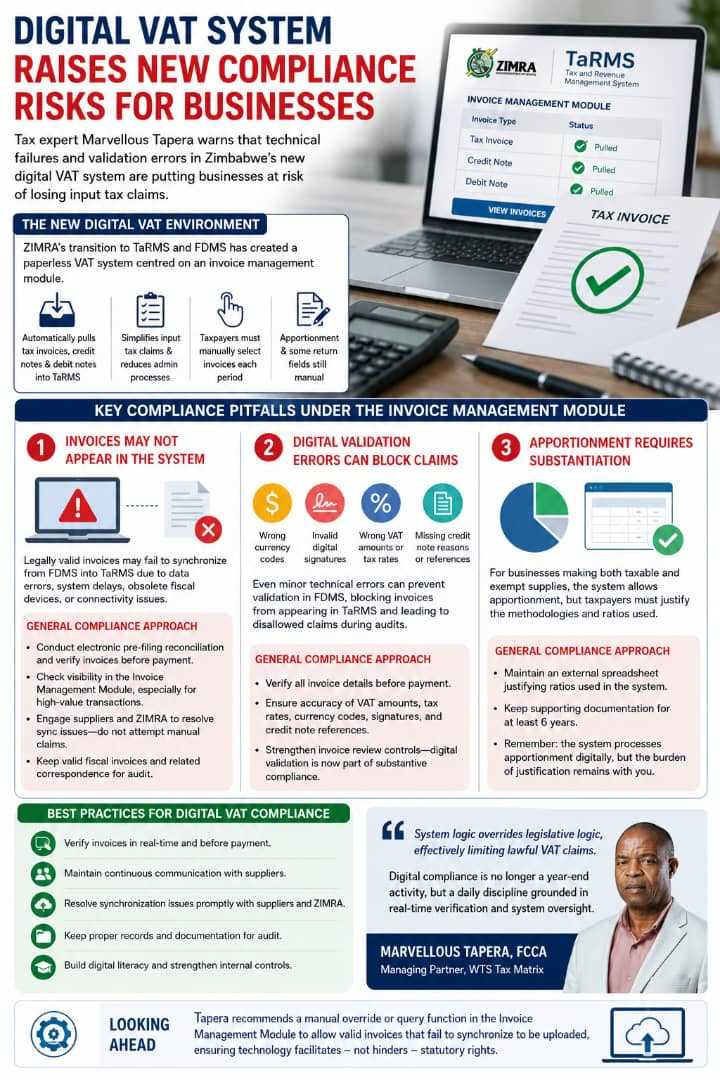

Businesses operating under Zimbabwe’s new digital Value Added Tax administration framework are facing emerging compliance risks as technical failures and system validation errors increasingly affect the processing of input tax claims, tax expert Marvellous Tapera has warned.

In an analysis titled Digital VAT Compliance in Situ: Critical Steps & Mistakes to Avoid, Tapera said the Zimbabwe Revenue Authority’s transition to the Tax and Revenue Management System and the Fiscalisation Data Management System has fundamentally reshaped VAT administration, shifting it to a largely paperless environment centred on an automated invoice management module.

Under the new framework, tax invoices, credit notes and debit notes are automatically transmitted into TaRMS to streamline input tax claims and reduce administrative burdens. However, Tapera noted that taxpayers still retain key manual responsibilities, including selecting invoices for each tax period, applying apportionment where taxable and exempt supplies coexist, and completing certain return fields.

While the system improves efficiency, he said it simultaneously raises the compliance threshold by requiring stronger digital literacy, continuous monitoring and proactive verification by businesses.

Tapera identified several compliance pitfalls arising from the invoice management module, warning that legally valid invoices may fail to qualify for VAT claims if they do not successfully synchronise from FDMS into TaRMS.

According to the analysis, synchronisation failures may stem from data transmission errors, backend integration delays, obsolete fiscal devices used by suppliers or unstable internet connectivity.

“In some cases, an invoice contains all required statutory features and validates on the portal without errors yet fails to appear in the Invoice Management Module due to technical lag,” Tapera said.

He warned that invoices not visible within the module cannot be manually claimed through the adjustments section, even where they comply fully with the VAT Act, potentially exposing taxpayers to penalties during audits.

Related Stories

Tapera described the emerging challenge as a situation in which “system logic overrides legislative logic,” effectively limiting otherwise lawful VAT claims.

To reduce exposure, he advised businesses to conduct electronic pre-filing reconciliations and verify invoices before making payments, particularly for high-value transactions. Taxpayers should also engage suppliers and the Zimbabwe Revenue Authority where invoices fail to synchronise instead of attempting manual claims outside the digital system.

The analysis further highlighted risks linked to digital validation requirements, noting that input tax claims may be rejected where invoices contain technical inaccuracies such as incorrect currency codes, invalid digital signatures, miscalculated VAT amounts, incorrect tax rates or incomplete credit note references.

Tapera said even minor technical discrepancies can prevent invoices from validating within FDMS, blocking their migration into TaRMS and ultimately resulting in disallowed claims during audits.

“Digital validation requirements now form part of substantive compliance,” he said, adding that businesses must strengthen internal invoice review controls to prevent technical disallowances.

He also cautioned taxpayers against assuming that VAT apportionment has become fully automated under the new system. Although the invoice management module allows apportionment within the platform, taxpayers remain responsible for justifying the methodologies and ratios applied.

Tapera recommended that businesses maintain external working papers, spreadsheets and supporting documentation for at least six years to substantiate allocations recorded through the portal.

While the invoice management module is expected to reduce manual VAT audits and enhance administrative efficiency, Tapera said digital compliance has effectively become “a daily discipline grounded in real-time verification and system oversight.”

He suggested authorities consider introducing a manual override or query function to allow taxpayers to upload valid fiscal invoices that fail to synchronise, arguing that technology should facilitate rather than restrict statutory tax rights.

Leave Comments