When African Sun Limited quietly exited the Victoria Falls Stock Exchange in April, the move initially appeared to be another post-pandemic restructuring by a hotel group still recovering from COVID-19 disruptions.

A closer financial examination now suggests something far more significant: the delisting may have exposed deep structural weaknesses within Zimbabwe’s flagship US-dollar-denominated exchange itself.

A plain-language analytical paper produced by Sizabantu Consulting argues that African Sun’s departure was not triggered by a single corporate failure but by a convergence of pressures that ultimately made remaining listed economically irrational.

Authored by financial strategist Kennedy Ndoro, the report concludes that the company’s market valuation had drifted far from the underlying value of its hotel assets, effectively trapping investors inside an illiquid market where price discovery had ceased to function properly.

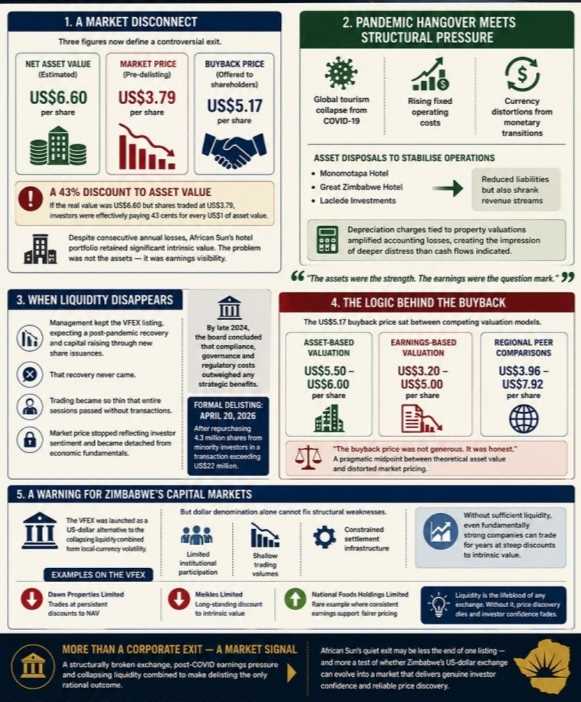

A Market Disconnect

Three figures now define one of Zimbabwe’s most debated corporate exits.

African Sun’s estimated net asset value stood at US$6.60 per share, while the stock traded at US$3.79 prior to delisting. The company ultimately offered shareholders US$5.17 per share in a buyback programme.

According to the analysis, the gap illustrated a market no longer reflecting economic reality.

“If the real value was US$6.60 but shares traded at US$3.79, investors were effectively paying 43 cents for every US$1 of asset value,” the report states.

Despite consecutive annual losses, the company’s portfolio — comprising some of Zimbabwe’s most recognisable hospitality assets — retained significant intrinsic value.

The problem, analysts argue, was not asset quality but earnings visibility.

Pandemic Hangover Meets Structural Pressure

The hospitality group faced lingering aftershocks from the global tourism collapse triggered by COVID-19, rising fixed operating costs and currency distortions linked to Zimbabwe’s monetary transitions.

In response, African Sun disposed of several assets, including the Monomotapa Hotel, Great Zimbabwe Hotel and Laclede Investments, seeking to stabilise operations and ease balance-sheet pressure.

While the disposals reduced liabilities, they also shrank revenue streams, leaving core operating costs largely unchanged.

The report further notes that depreciation charges tied to property valuations amplified reported accounting losses, creating the impression of deeper financial distress than operational cash flows may have indicated.

“The assets were the strength. The earnings were the question mark,” the analysis observes.

When Liquidity Disappears

Management initially maintained the VFEX listing in anticipation of a post-pandemic recovery that would restore investor confidence and enable capital raising through new share issuances.

That recovery never arrived.

Trading activity reportedly became so thin that entire sessions passed without transactions. Under such conditions, the market price ceased to represent active investor sentiment and instead became a static reference detached from economic fundamentals.

By late 2024, the board concluded that the compliance, governance and regulatory costs associated with remaining listed outweighed any strategic benefits.

African Sun formally delisted on April 20, 2026, after repurchasing 4.3 million shares from minority investors in a transaction exceeding US$22 million.

The Logic Behind the Buyback

The US$5.17 buyback price sat between competing valuation models.

Asset-based analysis placed the company’s value between US$5.50 and US$6.60 per share, while earnings-based approaches — reflecting recent losses — suggested a lower range of US$3.20 to US$5.00.

Comparisons with regional hospitality peers produced an even wider valuation spectrum of US$3.96 to US$7.92.

“The buyback price was not generous. It was honest,” the report concludes, describing the offer as a pragmatic midpoint between theoretical asset value and distorted market pricing.

A Warning for Zimbabwe’s Capital Markets

Beyond one company’s exit, the report raises broader questions about Zimbabwe’s capital market architecture.

The VFEX was launched as a US-dollar alternative to the Zimbabwe Stock Exchange, designed to attract foreign institutional investors wary of local-currency volatility.

Related Stories

However, the analysis argues that dollar denomination alone cannot compensate for structural weaknesses such as limited institutional participation, shallow trading volumes and constrained settlement infrastructure.

Without sufficient liquidity, analysts warn, even fundamentally strong companies can trade for years at steep discounts to intrinsic value.

The report points to Dawn Properties Limited and Meikles Limited as additional examples of firms that have experienced persistent valuation discounts, while National Foods Holdings Limited is cited as a rare case where consistent earnings supported closer alignment between market price and underlying value.

More Than a Corporate Exit

Ultimately, the paper frames African Sun’s departure not as a retreat but as a market signal.

“A structurally broken exchange, post-COVID earnings pressure and collapsing liquidity combined to make delisting the only rational outcome,” the analysis concludes.

For Zimbabwe’s financial markets, African Sun’s quiet exit may therefore represent less the end of one listing — and more a test of whether the country’s US-dollar exchange can evolve into a market capable of delivering genuine investor confidence and reliable price discovery.

The hospitality group faced lingering aftershocks from the global tourism collapse triggered by COVID-19, rising fixed operating costs and currency distortions linked to Zimbabwe’s monetary transitions.

In response, African Sun disposed of several assets, including the Monomotapa Hotel, Great Zimbabwe Hotel and Laclede Investments, seeking to stabilise operations and ease balance-sheet pressure.

While the disposals reduced liabilities, they also shrank revenue streams, leaving core operating costs largely unchanged.

The report further notes that depreciation charges tied to property valuations amplified reported accounting losses, creating the impression of deeper financial distress than operational cash flows may have indicated.

“The assets were the strength. The earnings were the question mark,” the analysis observes.

When Liquidity Disappears

Management initially maintained the VFEX listing in anticipation of a post-pandemic recovery that would restore investor confidence and enable capital raising through new share issuances.

That recovery never arrived.

Trading activity reportedly became so thin that entire sessions passed without transactions. Under such conditions, the market price ceased to represent active investor sentiment and instead became a static reference detached from economic fundamentals.

By late 2024, the board concluded that the compliance, governance and regulatory costs associated with remaining listed outweighed any strategic benefits.

African Sun formally delisted on April 20, 2026, after repurchasing 4.3 million shares from minority investors in a transaction exceeding US$22 million.

The Logic Behind the Buyback

The US$5.17 buyback price sat between competing valuation models.

Asset-based analysis placed the company’s value between US$5.50 and US$6.60 per share, while earnings-based approaches — reflecting recent losses — suggested a lower range of US$3.20 to US$5.00.

Comparisons with regional hospitality peers produced an even wider valuation spectrum of US$3.96 to US$7.92.

“The buyback price was not generous. It was honest,” the report concludes, describing the offer as a pragmatic midpoint between theoretical asset value and distorted market pricing.

A Warning for Zimbabwe’s Capital Markets

Beyond one company’s exit, the report raises broader questions about Zimbabwe’s capital market architecture.

The VFEX was launched as a US-dollar alternative to the Zimbabwe Stock Exchange, designed to attract foreign institutional investors wary of local-currency volatility.

However, the analysis argues that dollar denomination alone cannot compensate for structural weaknesses such as limited institutional participation, shallow trading volumes and constrained settlement infrastructure.

Without sufficient liquidity, analysts warn, even fundamentally strong companies can trade for years at steep discounts to intrinsic value.

The report points to Dawn Properties Limited and Meikles Limited as additional examples of firms that have experienced persistent valuation discounts, while National Foods Holdings Limited is cited as a rare case where consistent earnings supported closer alignment between market price and underlying value.

More Than a Corporate Exit

Ultimately, the paper frames African Sun’s departure not as a retreat but as a market signal.

“A structurally broken exchange, post-COVID earnings pressure and collapsing liquidity combined to make delisting the only rational outcome,” the analysis concludes.

For Zimbabwe’s financial markets, African Sun’s quiet exit may therefore represent less the end of one listing — and more a test of whether the country’s US-dollar exchange can evolve into a market capable of delivering genuine investor confidence and reliable price discovery.

Leave Comments